Roth IRA - Good For Many Retirement Savers

Are you considering your retirement savings options for 2006? Which should you choose – a Roth, or a Traditional IRA? In this entry we outline the features of each plan and analyze subtle distinctions between the two that lead us to the opinion that the Roth IRA is likely to prove the better option for a majority of today’s retirement savers.

Are you considering your retirement savings options for 2006? Which should you choose – a Roth, or a Traditional IRA? In this entry we outline the features of each plan and analyze subtle distinctions between the two that lead us to the opinion that the Roth IRA is likely to prove the better option for a majority of today’s retirement savers.

Background

As most investors know, the U.S. government provides individual taxpayers the opportunity to tuck away a limited amount of tax-advantaged savings each year through Individual Retirement Accounts (IRAs). For 2006 this amount remains fixed at $4,000. Added “catch-up” contributions (maximum of $500 in 2005 and $1,000 in 2006) are also available for savers aged 50 and older in the calendar year for which they make the contribution.

For most non self-employed savers, the Internal Revenue Service recognizes two distinct tax-advantaged savings options - the Traditional IRA and the Roth IRA. Savers can open Traditional and Roth plans at most financial institutions and the investment options and fees available through each are generally identical. Yet, there are distinct differences between Traditional and Roth IRAs that merit further attention. Let’s look at each in turn.

Traditional IRA

In most cases, savers contribute pre-tax money to traditional IRAs. In effect, contributions lower the saver’s taxable income in the tax year for which the money is contributed so that the saver realizes a tax benefit by making the contribution. These tax benefits are of greater value to higher income taxpayers than lower income taxpayers and can be calculated as the difference between what one would pay in taxes without making a contribution minus what one would pay in taxes by making a contribution.

All individuals under the age of 70 ½ with compensation are free to contribute up to the lesser of $4,000 or 100% of their compensation. Non-working spouses are free to contribute up to the maximum as well, though the combined contribution cannot exceed the couple’s combined compensation.

On the negative side, the deductibility of Traditional IRA contributions is limited as follows:

Individuals: For individuals covered by an employer’s retirement savings plan, Traditional IRA contributions are fully deductible for those with modified adjusted gross incomes (MAGI) up to $50,000. For MAGI of between $50,000 and $60,000, they’re partially deductible and for MAGI over $60,000 there is no tax deduction.

For individuals not covered by an employer’s retirement savings plan IRA deductibility is not limited by the saver’s modified adjusted gross income.

Married Filing Jointly: For couples filing jointly where one spouse is covered by an employer’s retirement plan, IRAs are fully deductible for modified adjusted gross income up to $150,000. MAGI of between $150,000 and $160,000 receives a partial tax deduction and MAGI over $160,000 renders IRA contribution non tax-deductible.

For couples where both spouses are covered under employer retirement plans, contributions to Traditional IRAs are fully deductible for MAGI up to $70,000, partially deductible between $70,000 and $80,000 and non-deductible for MAGI over $80,000.

For couples where neither is covered by an employer’s retirement plan, IRAs are fully deductible for all levels of MAGI.

From a practical perspective, modified adjusted gross income restrictions limit the economic benefit savers are likely to receive in the contribution year to a maximum of about 25% of their contribution. So, a contribution of $4,000 in 2005 will likely reduce your taxes by $1,000 at most.

Savers who withdraw funds prior to 59 ½ are subject to a penalty of 10% of the amount withdrawn as well as ordinary income taxes.

After the age of 59 ½ Traditional IRA savers are free to withdraw any, or all, funds from their account(s) without penalty, but all distributions are taxed as ordinary income in the year they are received. As such, most account holders attempt to postpone taking taxable distributions from their traditional IRAs for as long as possible. To limit this deferral, the U.S. government mandates that all Traditional IRA account-holders begin taking minimum required distributions from their accounts in the year in which they reach 70 ½. Initial mandatory minimum withdrawals amount to between 3.65% and 3.77% of the IRA prior-year balance and are based on the account value at the end of the prior year and actuarial life expectancy assumptions. Subsequent minimum required distributions increase in percentage terms, but may differ in absolute dollar amounts depending on the accounts prior-year balance.

Upon the death of the owner, Traditional IRAs pass to their appointed beneficiaries, typically outside the instructions of a will. Beneficiaries have an opportunity to stretch the tax-deferral aspects of the IRA as the minimum required distributions are re-calibrated based on their, typically longer.

Roth IRA

Unlike the Traditional IRA, contributions to a Roth IRA are not tax-deductible. Savers in these plans use after-tax money to fund their accounts, missing out on the upfront tax benefits accruing to those saving through Traditional IRAs. The benefit of the Roth IRA however is that not only does the principal grow tax-free during the life of the investment, but all withdrawals after age 59 ½ that have been invested at least five years are tax-free as well. From a practical perspective Traditional IRAs are tax-deferred assets while Roth IRAs are tax-free assets.

Furthermore, the fact that Roth assets have been taxed prior to contribution, benefits Roth IRA holders in two ways. First, there is no minimum distribution requirement imposed by the government, at any age. Second, contributions (though not gains on these contributions) can be withdrawn after 5 years without penalty, regardless of the saver’s age.

Individuals of any age with compensation (subject to income limits) can invest up to the minimum of $4,000 or 100% of their compensation in Roth IRAs and, like Traditional IRAs, non-working spouses can contribute an amount such that the couple’s total contribution does not exceed the lesser of $8,000 or their combined compensation. .

Of course, with any deal this good there have to be stipulations. The first is that single tax filers with adjusted gross incomes of between $95,000 and $115,000 and joint filers with AGIs between $150,000 and $160,000 are only eligible for partial contributions. Filers above these amounts are completely ineligible.

Second, to the extent contributions are withdrawn prior to the five year investment window, they will be assessed a 10% penalty. Also, to the extent investment gains are removed prior to age 59 1/2, they will be assessed a 10% penalty and taxed as ordinary income in the year they are withdrawn.

Exceptions to the 10% Penalty

There are a number of exceptions to the 10% penalty for early withdrawals from either Traditional or Roth IRAs. Specifically, the early withdrawal penalty does not apply to distributions that:

Occur because of the owner’s disability (see IRS Publication 590 for definitions and further details).

- Occur because of the owner’s disability (see IRS Publication 590 for definitions and further details).

- Occur because of the owner’s death.

- Are a series of “substantially equal periodic payments” made over the life expectancy of the owner.

- Are used to pay for un-reimbursed medical expenses that exceed 7 ½% of the owners adjusted gross income.

- Are used to pay medical insurance premiums, after the owner has received unemployment compensation for more than 12 weeks.

- Are used to pay the costs of a first-time home purchase (subject to a $10,000 lifetime limit).

- Are used to pay for qualified higher education expenses for the owner and/or eligible family members.

- Are used to pay back taxes due to an Internal Revenue Service levy placed against the IRA.

Before considering an early withdrawal however, we recommend you research these exceptions more carefully.

Traditional or Roth – Which is Right for You?

Assuming you’re eligible to invest in either plan, the decision on which is right for you hinges on a number of personal factors including your current and expected future tax rates, fluctuations in annual income, and overall ability to save. Additionally one should give thought to likely future tax rate changes and the value of implicit “options” afforded savers using the Roth plan. Let’s look at each factor in turn.

Current & Future Tax Rates: Assuming no changes to the tax code, it can be shown mathematically that if a saver’s current all-in tax rate is higher than his realized future tax rate, the Traditional IRA will yield a higher after-tax return, and conversely if a saver’s ordinary income tax rates are lower today than in the future, the Roth IRA will generate higher after-tax returns.

Given this, the question one needs to answer are as follows: “How much will I need to withdraw from my IRA annually in retirement to maintain the lifestyle I wish to live?” and “Assuming no changes to the tax code and inflationary trends of arguably 3% per year, what will my tax rate be in retirement?”

Many professionals argue that one needs 70%-80% of their pre-retirement income to sustain an equivalent lifestyle in retirement. If so, and you’re in you’re peak earnings years and closing in on retirement, a strong argument can be made for the Traditional IRA, as lower living expenses would drop you into lower tax rates in retirement. Yet, there are also many who argue that post-retirement income will need to be closer to 100% of pre-retirement income in order to afford ever-escalating healthcare costs and a more active retirement lifestyle than has historically been the norm.

One thing seems certain to us however; owing to inflation, the further out your retirement horizon, the more likely you’ll be pushed into a higher, not lower, tax bracket. This supports a Roth IRA as the preferred vehicle for younger savers.

Fluctuations in Annual Income: Job changes - some planned, some not - occur much more frequently today than they did just 15 years ago. With these disruptions most workers will likely experience significant fluctuations in their annual incomes before retirement. We advise savers to remain flexible over the years. When your tax rate is relatively low, take advantage of the Roth plan and when income is easier to come by shift to the Traditional IRA.

Ability to Save: While savers can choose to make contributions to either plan, recognize that a dollar saved in a Traditional IRA is not the same as a dollar saved in a Roth. In order to compare plans side-by-side, one must look at each from an “after-tax perspective” – and when this is done the Roth plan comes out as the more generous of the two.

Why? Think of it like this. Say you decide to maximize your IRA contribution with a $4,000 deposit. If you fund a Traditional IRA and you’re in the 25% tax bracket, you’re annual after-tax costs are $3,000. If instead you choose the Roth and invest $4,000 after-taxes, your out-of-pocket cost is an additional $1,000.

Then, at age 70 ½, you begin to draw down your IRA by $40,000 annually. Assuming you’re in an identical 25% tax bracket at that time, the Traditional IRA provides you with after-tax funds of $30,000 while the Roth IRA allows you to keep the entire $40,000.

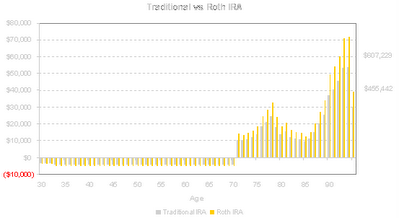

The chart below presents a hypothetical case showing the lifetime after-tax cash-flows for two investors – one who contributes $4,000 each year to a Traditional IRA and one who contributes the same amount to a Roth. Both are assumed to invest in identical portfolios throughout their lives.

Though each contributed a nominal $4,000 annually prior to retirement, the Roth IRA holder contributed 33% more after-tax. In retirement she receives 33% more after-tax income each year and ends life with a residual value 33% higher as well. In short, The Roth allows those who have the resources to build a larger pool of after-tax savings for retirement.

Likely Future Tax Rates: It’s almost certain the U.S. (and state) tax codes will change over the coming decades and, in our opinion, an aging baby-boomer generation and ever-increasing government deficit spending imply that changes to tax rates will be up, not down. If so, the better savings option, as noted above, is the Roth plan.

Some financial professionals argue that investors should retain funds in both types of plan as a “hedge” against future rate changes. In our opinion, this is probably not a bad idea, especially if you already have a sufficiently funded Traditional or Rollover IRA.

Implicit Options within the Roth IRA: We believe one of the most appealing, but often overlooked, aspects of the Roth IRA is that it provides the saver with an “option” to partially withdraw funds from the plan prior to retirement without penalty. Recall that after 5 years of investment the saver can withdraw up to the original contribution amount (though not earnings on those contributions) without penalty. This is an attractive option to have, and one not afforded Traditional IRA investors.

Conversions to a Roth IRA

As you’ve probably guessed, our view is that the Roth IRA is likely to be the preferred tax-advantaged investment vehicle for most retirement savers. In fact, Roth IRAs have become extremely popular savings vehicles over the first seven years of their existence and many individuals have taken an opportunity to convert all, or a part, of their existing Traditional IRAs to Roths.

Here’s what you need to know if you’d like to convert an existing Traditional or Rollover IRA to a Roth. First, you can only do a conversion in a year where your adjusted gross income (AGI), before the conversion amount is less than $100,000. This limitation is regardless of whether you’re filing taxes as “single”, “married filing jointly” or “head-of-household”. Those “married filing separately” are not allowed to undertake a conversion at all.

Second, if you choose to undertake a conversion the 10% penalty for early withdrawal from a Traditional IRA will be waived, but your conversion will be treated as ordinary income for tax purposes in the year of the conversion.

Third, if part of your conversion is of prior non-deductible contributions (after-tax) they will not be taxed on conversion, as they’re already after-tax assets.

Fourth, if you choose to use part of your existing IRA to pay taxes on the conversion, you’ll likely do so by making a withdrawal from your existing IRA prior to converting the remainder. These funds will be assessed the 10% early-withdrawal penalty (in the case of withdrawal of non-deductible contributions) and ordinary income taxes (in the case of withdrawal of deductible contributions).

Finally, once a Traditional IRA has been converted none of these funds can be withdrawn from the Roth IRA within the first five years without a 10% penalty. After five years, any or all of these contributed funds can be withdrawn without penalty.

Feel free to contact us at Pariveda Investment Management (1-888-688-5780) if you have any questions.